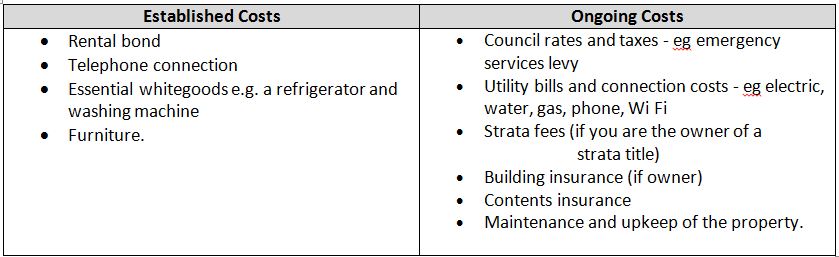

Major Costs

Established costs- These are one-off costs that are involved in setting up your new place to live.

Ongoing costs- These are recurring costs typically associated with mainly maintenance.

Ongoing costs- These are recurring costs typically associated with mainly maintenance.

6 Top Tips To Staying Financially Problem Free

1. Create a realistic budget and ensure you follow it.

This means every so often to be checking your budget against your actual spending patterns and readjusting your figures and spending habits accordingly.

2. Don't impulse buy.

When you see something you hadn't planned to buy and don't actually need, don't purchase it on the spot. Go home and think it over. It's less likely you'll return to buy it after having had a chance to think it over.

3. Don’t buy something just because it’s on sale.

Buying a $450 item on sale for $340 isn’t a $110 savings if you didn’t need the item to begin with. It’s spending $340 unnecessarily. (And it may not have been a real sale – some stores mark items down almost immediately, to make people think they’re getting a bargain.)

4. Avoid large rent or house payments.

Obligate yourself only for what you can now afford and increase your mortgage payments only as your income increases. Consider refinancing your house if your payments are unwieldy.

5. Avoid co-signing or guaranteeing a loan for someone.

Your signature obligates you as if you were the primary borrower. You can’t be sure that the other person will pay.

6. Don’t make high-risk investments, such as investments in speculative real estate, penny stocks and junk bonds.

Invest conservatively, opting for certificates of deposit, money market funds, and government bonds.

This means every so often to be checking your budget against your actual spending patterns and readjusting your figures and spending habits accordingly.

2. Don't impulse buy.

When you see something you hadn't planned to buy and don't actually need, don't purchase it on the spot. Go home and think it over. It's less likely you'll return to buy it after having had a chance to think it over.

3. Don’t buy something just because it’s on sale.

Buying a $450 item on sale for $340 isn’t a $110 savings if you didn’t need the item to begin with. It’s spending $340 unnecessarily. (And it may not have been a real sale – some stores mark items down almost immediately, to make people think they’re getting a bargain.)

4. Avoid large rent or house payments.

Obligate yourself only for what you can now afford and increase your mortgage payments only as your income increases. Consider refinancing your house if your payments are unwieldy.

5. Avoid co-signing or guaranteeing a loan for someone.

Your signature obligates you as if you were the primary borrower. You can’t be sure that the other person will pay.

6. Don’t make high-risk investments, such as investments in speculative real estate, penny stocks and junk bonds.

Invest conservatively, opting for certificates of deposit, money market funds, and government bonds.